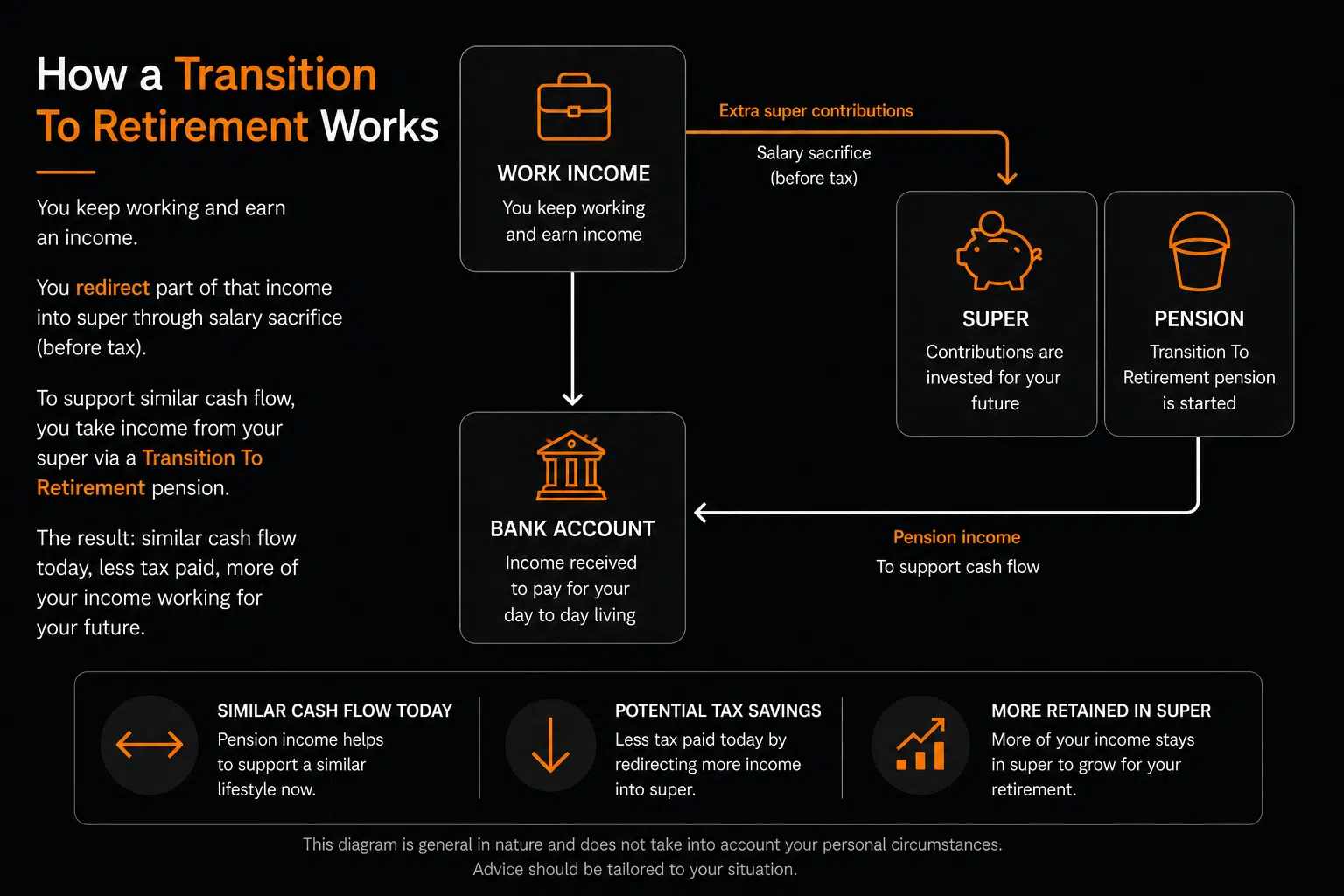

✓ Potentially contribute more into super

✓ Maintain similar cash flow

✓ Improve tax efficiency

✓ Create greater flexibility before retirement

Book an initial conversation to explore whether a Transition To Retirement strategy may suit your situation.