Debt Recycling

Debt Recycling Strategy on the Northern Beaches

Use your home loan to build long term wealth in a structured and tax effective way.

A debt recycling strategy is one of the most effective ways to build wealth using your existing home loan.

Rather than focusing on paying down debt alone, this approach allows you to gradually convert non-deductible debt into investment debt, while building a long-term investment portfolio at the same time.

For many clients, the challenge is not whether debt recycling works, but how to structure it properly so it is sustainable, tax effective, and aligned with their broader financial plan.

What is a debt recycling strategy

A debt recycling strategy is a way of using your existing home loan to build investments in a more structured and tax effective way.

Instead of focusing only on paying down your mortgage, the structure is adjusted so that over time, non-deductible debt is reduced and replaced with investment debt.

This allows you to build an investment portfolio alongside your loan, while improving your overall tax position.

The focus is not just on growth, but on creating a structure that supports cash flow and long term sustainability.

In some cases, available equity can also be used to begin investing sooner, before continuing the recycling process over time.

Reduces non-deductible debt ✔

Builds an investment portfolio ✔

Improves tax efficiency ✔

Improves cash flow and sustainability ✔

How debt recycling works in practice

A debt recycling strategy works by restructuring your home loan and using your existing cash flow more effectively.

The focus is not just on reducing debt, but improving how that debt is structured over time.

This typically involves splitting your loan, reducing non-deductible debt, then re-borrowing that amount to invest and repeating the process over time.

Over time, this builds an investment portfolio alongside your loan, with a gradual shift towards more efficient, tax effective debt.

Importantly, total debt may stay the same or increase. The goal is to reduce non-deductible debt and replace it with investment debt, while maintaining cash flow.

1) Restructure your home loan

Split your loan so different parts can be managed separately

2) Reduce non-deductible debt

Use cash flow to pay down your home loan

3) Re-borrow to invest

Convert that amount into a separate investment loan

4) Repeat over time

Build investments while improving your structure

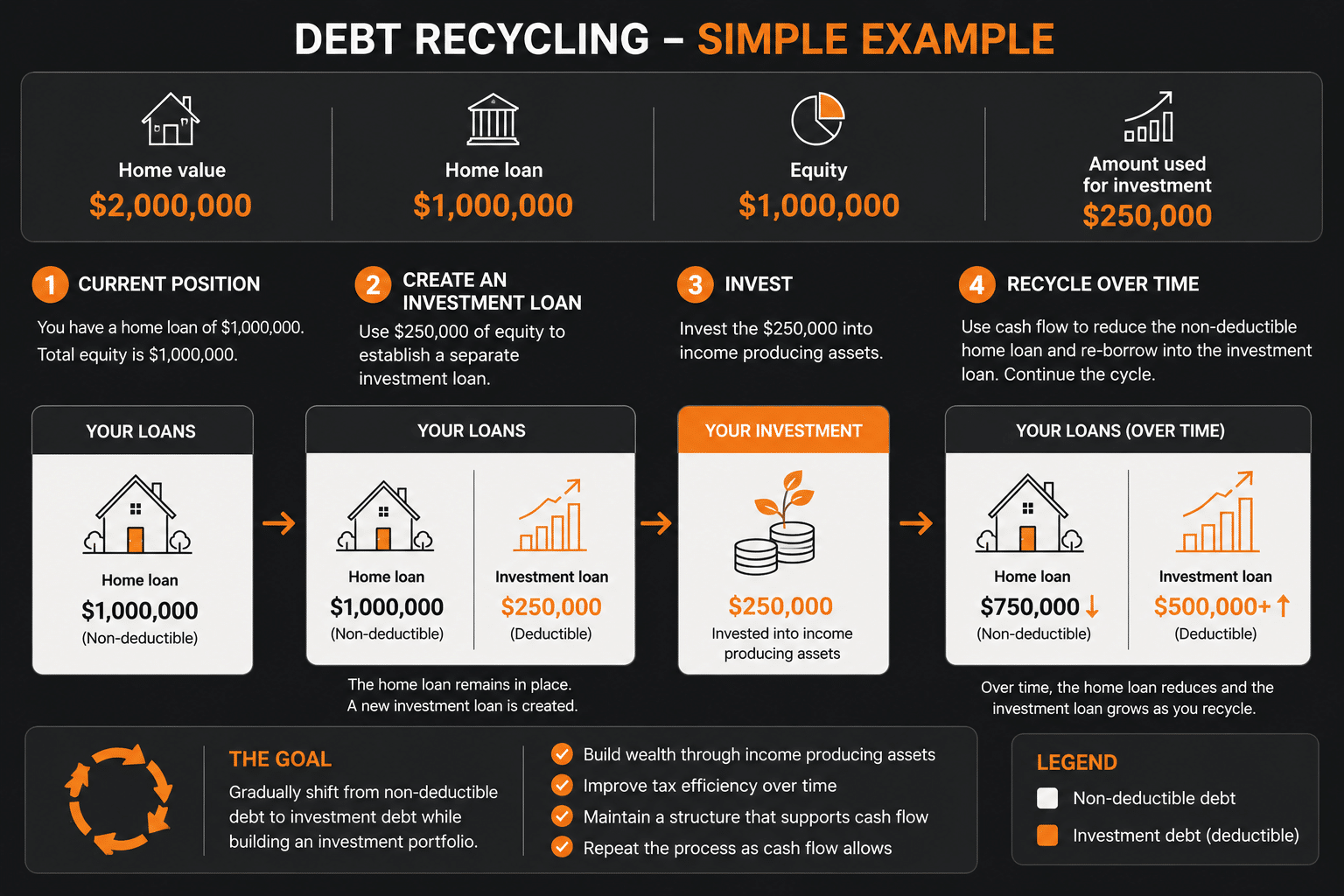

A simple example of how debt recycling works

To make this more practical, here is a simplified example of how a debt recycling strategy may be structured over time.

Home value: $2,000,000

Home loan: $1,000,000

Equity: $1,000,000

Amount used for investment: $250,000

In this example, a portion of the equity is used to establish an investment split.

Those funds are then invested into income producing assets, while the remaining home loan continues to be managed separately.

Over time, as cash flow allows, portions of the non-deductible loan can be reduced and re-borrowed into the investment split, continuing the recycling process.

This results in a growing investment portfolio, a gradual shift from non-deductible to investment debt, and improved tax efficiency over time.

The focus is on maintaining a structure that supports cash flow, rather than relying purely on growth.

What this looks like over time

Over time, the structure begins to shift.

Instead of simply reducing your home loan, you are building an investment portfolio alongside your debt.

Non-deductible debt is gradually reduced and replaced with investment debt, improving the overall efficiency of your position.

Importantly, your total debt may not reduce as quickly in the early years.

However, you are building assets at the same time, creating a stronger long term structure.

Is debt recycling right for you

A debt recycling strategy is not right for everyone.

It may be appropriate if you:

You have stable income

You have surplus cash flow

You are comfortable investing over the long term

You want to improve the structure of your finances

The key is ensuring the strategy is structured in a way that you can maintain over time.

Estimate how gradually converting home loan debt into investment debt may impact your wealth over time.

Actual outcomes depend on your loan structure, interest rates, repayments, tax position, investment returns, fees, income, borrowing capacity and personal circumstances. This tool does not provide personal financial advice and should not be relied on as a prediction of your actual outcome.

Start with a structured approach

The first step is understanding how a debt recycling strategy would apply to your situation and how it fits into your broader financial plan.

From there, we can map out the structure and next steps.

You can also learn more about investment loan interest deductibility through the ATO, as well as the risks and considerations associated with borrowing to invest through ASIC Moneysmart.

We warmly welcome new clients and our door is always open.

Let us take the stress and hassle out of managing your financial goals so you can focus on the important stuff.